Perspectives from the acquired

Capitaland acquisition of Ascendas Singbridge

From a high level perspective, Temesek holdings and capitaland is doing a merger via swapping of shares. Capitaland gains control over the units of A-REIT, I trust H trust, and property development arm of Ascendas Sing bridge. Temesek gains a controlling stake in the Capitaland cash cow. There is no direct impact on Ascendas India trust and ascendas REIT as the controlling shareholder TH stays the same, amid shrouded by an additional corporate veil.

18.14% of my portfolio is exposed to ascendas singbridge. (Ascendas India trust and Ascendas REIT). Although I did not deliberately structure it to be significantly exposed to one single sponsor , it could be a potentially unexpected windfall if capitaland shareholders decide to approve this acquisition and the acquirer makes a tender offer for the remaining I trust and A REIT units (In capitaland shares or cash). This is nonetheless speculation as firm details can only be provided after shareholders voted for the Capitaland EGM, and subsequent corporate actions to be announced by the respective Ascendas listed entities.

Ascendas REIT is my first active lump sum position for my investment journey since I started active investing at 30 Dec 16. I bought it at the onset of the first US interest hike (14 Dec 16) whereby everyone is proclaiming the doom of REITS and ignoring the huge accumulated war-chest position of Ascendas REIT. It is one of the rare times there is a clear case for undervaluation of REITS. It is currently one of my top performer at 34.68% return inclusive of dividends. Nonetheless, the uncertain outlook of its UK properties following BREXIT and its increasing geographical allocation to overseas properties (harder to monitor) held me back from averaging up since then.

The significant part of my portfolio exposure stems from Ascendas I trust. Despite not named as a REIT, it's gearing and capital structure is similar and the expertise and management running the trusts are focused and competent . It's main attraction is it's strong growth prospects in a strong market economy and exceptional favorable tenant demographics. The profitability, strategic location at special economic zone, and cash generating prowess of this trust (winning several prizes to illustrate the point) is the main reason I have been accumulating it despite it trading above tangible book value.

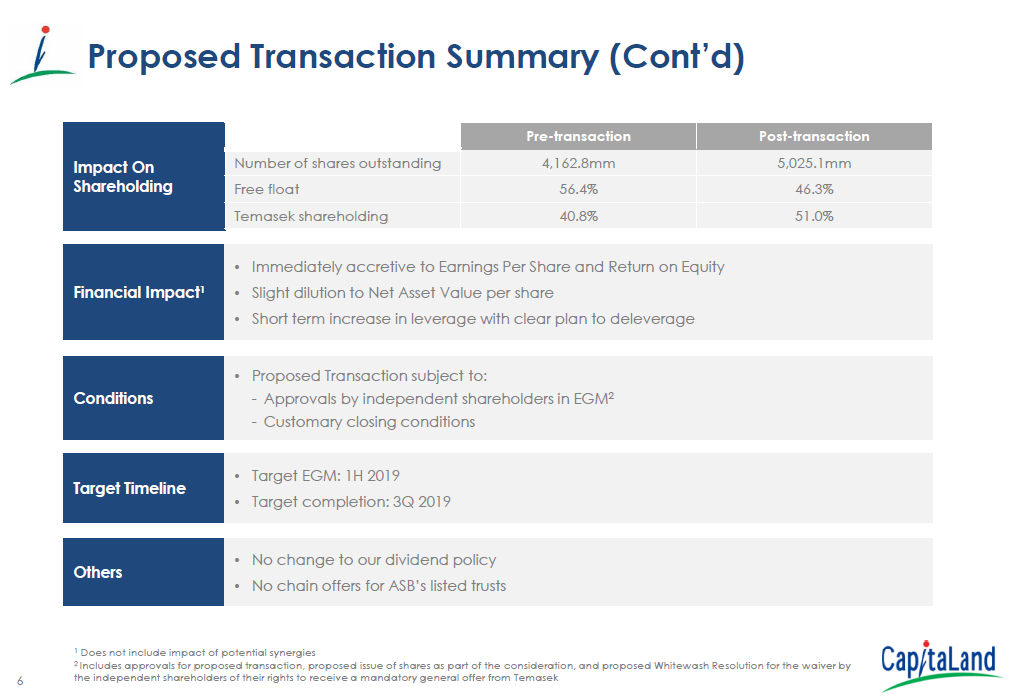

As of this time, from an I trust and A REIT unit-holder perspective, I don't see any direct impact on my underlying investments stemming from this corporate event. There might be renewed interest from the market to review the underlying Sing bridge listed entities once the catalyst / Capitaland EGM results are out. It might be a worthwhile proposition to accumulate these counter while I patiently wait for the results of capitaland EGM to be out by 1H 2019.

Links

https://risknreturns.com/2019/01/14/initial-thoughts-on-the-capitaland-ascendas-singbridge-acquisition/

https://risknreturns.com/2019/01/14/initial-thoughts-on-the-capitaland-ascendas-singbridge-acquisition/

https://blog.seedly.sg/capitaland-proposed-acquisition-ascendas-singbridge-sgx-c31/

https://financialhorse.com/capitaland-ascendas-singbridge/

https://www.straitstimes.com/business/companies-markets/capitaland-to-buy-temasek-unit-ascendas-singbridge-in-11b-deal-creating

https://www.straitstimes.com/business/companies-markets/capitaland-to-buy-temasek-unit-ascendas-singbridge-in-11b-deal-creating

Comments

Post a Comment